Things about Mortgage Investment Corporation

Things about Mortgage Investment Corporation

Blog Article

8 Easy Facts About Mortgage Investment Corporation Described

Table of ContentsThe 10-Minute Rule for Mortgage Investment CorporationExamine This Report about Mortgage Investment CorporationThe 9-Second Trick For Mortgage Investment CorporationMortgage Investment Corporation Can Be Fun For AnyoneThe 6-Second Trick For Mortgage Investment Corporation

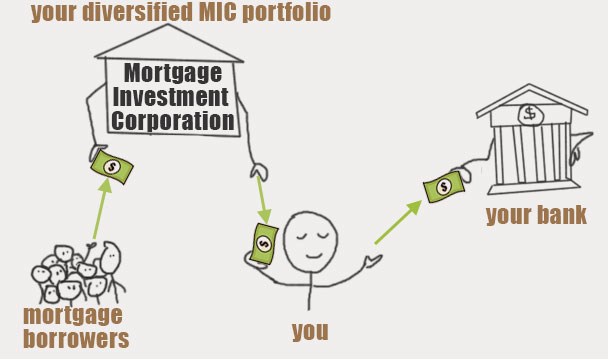

A Mortgage Financial Investment Company (MIC) gives a passive means to spend in the real estate market, alleviating the time and danger of investing in individual home mortgages. The MIC is taken care of by a supervisor who is liable for all facets of the company's operations, consisting of the sourcing of ideal home loan financial investments, the analysis of home loan applications, and the arrangement of applicable rate of interest prices, terms and problems, guideline of lawyers, mortgage portfolio and general management.100% of a MIC's yearly take-home pay, as verified by exterior audit, be dispersed to its shareholders in the kind of a returns - Mortgage Investment Corporation. This dividend is tired as interest revenue in the hands of shareholders, avoiding dual tax. A MIC's profits are comprised of mortgage rate of interest and charge earnings. Expenditures are predominantly consisted of administration charges, audit and various other expert charges, and car loan interest if the MIC employs debt in enhancement to share resources.

A MIC is typically widely held. At the very least 50% of a MIC's assets need to be comprised of household home mortgages and/or cash money and guaranteed deposits at copyright Down payment Insurance Corporation participant monetary institutions.

The world of investing teems with choices. Many people are familiar with the much more conventional techniques of investing, such as supplies and bonds. Mortgage Investment Corporation. Choice spending now enables financiers to use markets that exist beyond the banks. There are lots of distinctions in between these traditional investing and option investing techniques, and with these distinctions come many institutions and companies to select from.

Getting The Mortgage Investment Corporation To Work

Let's simply claim, the differences are lots of, and it's these distinctions that are essential when it concerns recognizing the value of diversifying your financial investment profile. The main resemblance between a bank and a MIC is the idea of merging funds with each other to expand the fund itself, then selling sections of the fund to financiers.

To increase on the previous factor associated with their terms, with a difference in term sizes comes rates of interest modifications. When your financial investments are bound in an in a bank-related home loan fund, the size of the term can suggest losing cash with time. Rates of interest can alter in the markets, and the rate of interest made on these home mortgages might not as a result of fixed-rate fundings.

Mortgage Investment Corporation Can Be Fun For Everyone

A home loan swimming pool managed by an MIC will frequently pay dividends month-to-month as opposed to quarterly, like bank supplies. This can be of higher advantage to capitalists searching for a passive revenue stream. Typically, when you choose to purchase a home loan pool handled by a credible MIC, you're using their understanding.

Any time you concentrate your focus into a niche market, you're going to be extra acquainted and experienced than someone who has to put on many hats. MICs do not response to the exact same regulatory agencies as financial institutions, and due to this, they have more freedom. Banks can't take the very same risks that private firms or investors can profit from.

The kind of residential property or task that MICs and exclusive home loan funds are associated with usually loss under the umbrella of realty advancement or building and construction. This my sources is many thanks to the shorter approval times related to home mortgage pools with MICs rather than banks. There are absolutely advantages to buying even more standard approaches.

Mortgage Investment Corporation - Questions

That makes actual estate a strong service financial investment, specifically in this modern period. A home loan financial investment corporation can let you take advantage of their demands and invest in a flourishing organization that would certainly allow you to gain some major returns.

When someone wants to acquire a residential or commercial property, they generally take a mortgage from a bank or some various other lending firm. The returned money consists of rate of interest, which is the primary way the lender makes cash.

MIC, additionally lends money to borrowers. Unlike standard lending institutions, MICs also let financiers invest in their company to make a share of the rate of interest earned. The following steps are involved in the organization process of a MIC.

The Greatest Guide To Mortgage Investment Corporation

For the next action, the financier connects with a MIC and asks to buy their business. If you fulfill the minimum financial investment standards for the MIC you're choosing, you must have the ability to obtain your financial investment with quickly. You can discover any type of MIC's minimal financial investment requirements on their internet site.

Report this page